Superannuation can be a tax-effective way of saving for retirement and it is well known that employers are required to contribute to their employee’s superannuation funds (Funds) separate to taxable income.[1] However, taxes still apply to all aspects of Funds. The rate used differs depending on what is being taxed.

The two (2) main categories of tax applied to a person’s Fund are on:

- before-tax (Concessional) contributions (Contributions Tax); and

- Fund’s investment earnings, for example, interest and dividends (Investment Tax).

This article discusses the Contributions and Investment Taxes and provides examples of how they are applied.

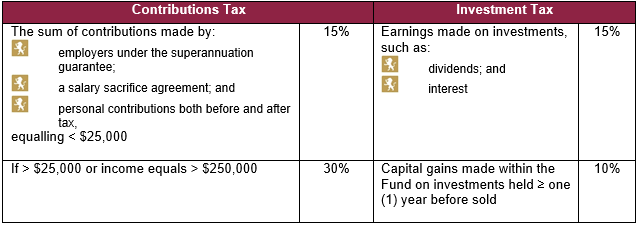

The table below provides an overview.

For a discussion about tax on income is above $250,000, please see our article on Division 293 tax.

Contributions Tax

A person’s Contributions Tax is determined by assessing the sum of:

- employer contributions under the superannuation guarantee to a Fund in any given financial year;[2]

- any personal Concessional contributions; and

- any contributions made by your employer through a salary sacrifice agreement.[3]

Any contributions from salary sacrifice agreement are included in a person’s salary amount when assessing their superannuation guarantee of 9.5%.[4] When a person’s total Concessional contributions are below $25,000 (Cap), the Tax rate is fifteen percent (15%) and is applied through a person’s Fund.[5] After-tax (Non-Concessional) contributions that do not result in the total exceeding the Cap have already been taxed and therefore are not dutiable.[6]

For example, you earn $76,000 per year but only receive $66,000 with $10,000 going to your Fund under a salary sacrifice agreement. Your employer still contributes the required nine and a half percent (9.5%) of your whole salary to your Fund which amounts to $7,220 per year. You add another $3,000 in Non-Concessional contributions in a financial year. The total contributed to your Fund is $20,220 for that financial year which is below the Cap. Therefore, the total taken from your Fund under the Contributions Tax is $3,033.

Investment Tax

Generally, interest and dividends earnt on superannuation investments (Earnings) attracts the Contributions Tax of fifteen percent (15%).[7] If an investment held within the Fund for at least one (1) year attracts capital gains tax (CGT) when sold, the tax rate may be discounted to ten percent (10%).[8] If a person is aged 60 or over and the Earnings could be categorised as an income stream, such as a pension, no tax is applied.[9]

For example, dividends received from shares across your Fund amounts to $2,000 over a financial year. Additionally, within the same financial year, you sold a property that had been held in your Fund for three (3) years that results in a capital gain of $10,000.[10] Your total Earnings are $12,000 but they are taxed at different rates. The dividends attract the Contributions Tax of fifteen percent (15%) resulting in $300 dutiable. The property sale also attracts the Contributions Tax but is liable to the CGT deduction limiting it to ten percent (10%) meaning $1,000 is dutiable. Therefore, $1,300 is taken from your Fund under the Investment Tax.

Takeaways

A person’s superannuation is most commonly taxed on contributions made into and Earnings made within their Fund. Contributions below the Cap will attract a tax of fifteen percent (15%). Earnings attract the same tax rate. However, the tax rate on capital gains made within a Fund on investments held for at least one (1) year can be deducted to ten percent (10%).

Links and further references

Legislation

Income Tax Assessment Act 1997 (Cth)

Income Tax Rates Act 1986 (Cth)

Income Tax Assessment Regulations 1997 (Cth)

Superannuation (Excess Non-Concessional Contributions Tax) Act 2007 (Cth)

Superannuation Guarantee (Administration) Act 1992 (Cth)

Superannuation Industry (Supervision) Act 1993 (Cth)

Further information about tax obligations

If you need assistance with your tax obligations, contact us for a confidential and obligation-free discussion:

Malcolm Burrows B.Bus.,MBA.,LL.B.,LL.M.,MQLS.

Legal Practice Director

T: +61 7 3221 0013 (preferred)

M: +61 419 726 535

E: mburrows@dundaslawyers.com.au

Disclaimer

This article contains general commentary only. You should not rely on the commentary as legal advice. Specific legal advice should be obtained to ascertain how the law applies to your particular circumstances.

[1] Superannuation Guarantee (Administration) Act 1992 (Cth).

[2] Income Tax Assessment Act 1997 (Cth) s 291.25(1); Superannuation Industry (Supervision) Act 1993 (Cth) s 45.

[3] Income Tax Assessment Act 1997 (Cth) s 291.25(1); Superannuation Guarantee (Administration) Act 1992 (Cth) s 15A(1).

[4] Superannuation Guarantee (Administration) Act 1992 (Cth) s 19(1)-(2).

[5] Income Tax Assessment Act 1997 (Cth) s 295.10; Income Tax Rates Act 1986 (Cth) s 26(1)(a).

[6] Income Tax Assessment Act 1997 (Cth) ss 290.150, 292.80, 292.90, 295.125; Superannuation (Excess Non-Concessional Contributions Tax) Act 2007 (Cth) s 4.

[7] Income Tax Assessment Act 1997 (Cth) ss 280.20(2)(3), 280.30(4).

[8] Income Tax Assessment Act 1997 (Cth) ss 115.5, 115.10(b), 115.15, 115.20, 115.25, 115.100(b)(i).

[9] Income Tax Assessment Act 1997 (Cth) 280.20(4), 280.25, 280.30(2), 307.200; Income Tax Assessment Regulations 1997 (Cth) reg 307.200.02.

[10] Income Tax Assessment Act 1997 (Cth) ss 100.35, 100.40(2), 100.45.

Related insights into tax law

-

What is my superannuation taxed at?

This article summarises the Australian Privacy Principles (APPs) and the importance of having a data destruction policy (DDP) in place. It outlines the steps to take when destroying or deidentifying personal and sensitive information, and the consequences of not doing so.

-

Division 293 tax – explained

Learn about the Division 293 Tax, a 15% additional tax on pre-tax super contributions over $25,000 for individuals earning over $250,000. Understand the criteria, how it is applied and related tax articles.

-

Transfer duty exemption for small business restructuring

The Queensland Commissioner of State Revenue has issued a public ruling outlining potential exemptions from transfer duty for eligible small business entities undergoing a restructuring. Get the full details of the ruling, its implications and eligibility requirements here.

-

Division 7A ITTA 1936 (Cth) – compliance & consequences

This article provides an overview of Division 7 of the Income Tax Assessment Act 1936 (Cth), covering advances of moneys and loans between private companies and its shareholders/associates, exceptions to these, and requirements for a compliant Division 7A loan agreement. The implications of failing to have a compliant agreement are explained in this article.

-

Value shifting in commercial transactions explained

Value shifting is an important tax consideration in Australia. This article outlines the general regime and exemptions, as well as Australian Taxation Office (ATO) resources for guidance.

-

Which entities qualify for the R&D Tax Incentive?

Companies can benefit Australia through the Research and Development Tax Incentive (R&D Tax Incentive), which offers a tax offset. Eligibility depends on an entity’s status. Trusts can also access the incentive via Trust Rollover or licence agreement.

-

Transfer duty implications for loans

Transfer Duty in Queensland: does it apply to loans? This article explores the Duties Act 2001 (Qld) and what constitutes a dutiable transaction and dutiable property. Find out if transfer duty applies to loans and learn more about the implications of loan agreements.

-

Transfer duty and issuing units in a unit trust

Discover how Queensland transfer duty is applied to dutiable transactions and what it means for your trust. Click through to the article for a comprehensive guide to the Duties Act 2001 (Qld).

-

Eligibility criteria for the Trust Restructure Rollover

Thinking of restructuring your trust for some reason? While there are certainly a number of commercial benefits in transitioning from a trust into a company, a common pitfall is failing to acknowledge potential liability for Capital Gains Tax (CGT) or address potential liability for state based transfer duty (Stamp Duty).