Superannuation can be a tax-effective way of saving for retirement and it is well known that employers are required to contribute to their employee’s superannuation funds (Funds) separate to taxable income.[1] However, taxes still apply to all aspects of Funds. The rate used differs depending on what is being taxed.

The two (2) main categories of tax applied to a person’s Fund are on:

- before-tax (Concessional) contributions (Contributions Tax); and

- Fund’s investment earnings, for example, interest and dividends (Investment Tax).

This article discusses the Contributions and Investment Taxes and provides examples of how they are applied.

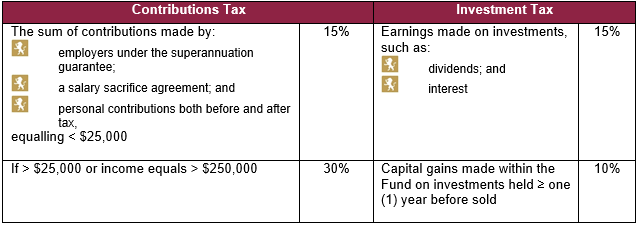

The table below provides an overview.

For a discussion about tax on income is above $250,000, please see our article on Division 293 tax.

Contributions Tax

A person’s Contributions Tax is determined by assessing the sum of:

- employer contributions under the superannuation guarantee to a Fund in any given financial year;[2]

- any personal Concessional contributions; and

- any contributions made by your employer through a salary sacrifice agreement.[3]

Any contributions from salary sacrifice agreement are included in a person’s salary amount when assessing their superannuation guarantee of 9.5%.[4] When a person’s total Concessional contributions are below $25,000 (Cap), the Tax rate is fifteen percent (15%) and is applied through a person’s Fund.[5] After-tax (Non-Concessional) contributions that do not result in the total exceeding the Cap have already been taxed and therefore are not dutiable.[6]

For example, you earn $76,000 per year but only receive $66,000 with $10,000 going to your Fund under a salary sacrifice agreement. Your employer still contributes the required nine and a half percent (9.5%) of your whole salary to your Fund which amounts to $7,220 per year. You add another $3,000 in Non-Concessional contributions in a financial year. The total contributed to your Fund is $20,220 for that financial year which is below the Cap. Therefore, the total taken from your Fund under the Contributions Tax is $3,033.

Investment Tax

Generally, interest and dividends earnt on superannuation investments (Earnings) attracts the Contributions Tax of fifteen percent (15%).[7] If an investment held within the Fund for at least one (1) year attracts capital gains tax (CGT) when sold, the tax rate may be discounted to ten percent (10%).[8] If a person is aged 60 or over and the Earnings could be categorised as an income stream, such as a pension, no tax is applied.[9]

For example, dividends received from shares across your Fund amounts to $2,000 over a financial year. Additionally, within the same financial year, you sold a property that had been held in your Fund for three (3) years that results in a capital gain of $10,000.[10] Your total Earnings are $12,000 but they are taxed at different rates. The dividends attract the Contributions Tax of fifteen percent (15%) resulting in $300 dutiable. The property sale also attracts the Contributions Tax but is liable to the CGT deduction limiting it to ten percent (10%) meaning $1,000 is dutiable. Therefore, $1,300 is taken from your Fund under the Investment Tax.

Takeaways

A person’s superannuation is most commonly taxed on contributions made into and Earnings made within their Fund. Contributions below the Cap will attract a tax of fifteen percent (15%). Earnings attract the same tax rate. However, the tax rate on capital gains made within a Fund on investments held for at least one (1) year can be deducted to ten percent (10%).

Links and further references

Legislation

Income Tax Assessment Act 1997 (Cth)

Income Tax Rates Act 1986 (Cth)

Income Tax Assessment Regulations 1997 (Cth)

Superannuation (Excess Non-Concessional Contributions Tax) Act 2007 (Cth)

Superannuation Guarantee (Administration) Act 1992 (Cth)

Superannuation Industry (Supervision) Act 1993 (Cth)

Further information about tax obligations

If you need assistance with your tax obligations, contact us for a confidential and obligation-free discussion:

Malcolm Burrows B.Bus.,MBA.,LL.B.,LL.M.,MQLS.

Legal Practice Director

T: +61 7 3221 0013 (preferred)

M: +61 419 726 535

E: mburrows@dundaslawyers.com.au

Disclaimer

This article contains general commentary only. You should not rely on the commentary as legal advice. Specific legal advice should be obtained to ascertain how the law applies to your particular circumstances.

[1] Superannuation Guarantee (Administration) Act 1992 (Cth).

[2] Income Tax Assessment Act 1997 (Cth) s 291.25(1); Superannuation Industry (Supervision) Act 1993 (Cth) s 45.

[3] Income Tax Assessment Act 1997 (Cth) s 291.25(1); Superannuation Guarantee (Administration) Act 1992 (Cth) s 15A(1).

[4] Superannuation Guarantee (Administration) Act 1992 (Cth) s 19(1)-(2).

[5] Income Tax Assessment Act 1997 (Cth) s 295.10; Income Tax Rates Act 1986 (Cth) s 26(1)(a).

[6] Income Tax Assessment Act 1997 (Cth) ss 290.150, 292.80, 292.90, 295.125; Superannuation (Excess Non-Concessional Contributions Tax) Act 2007 (Cth) s 4.

[7] Income Tax Assessment Act 1997 (Cth) ss 280.20(2)(3), 280.30(4).

[8] Income Tax Assessment Act 1997 (Cth) ss 115.5, 115.10(b), 115.15, 115.20, 115.25, 115.100(b)(i).

[9] Income Tax Assessment Act 1997 (Cth) 280.20(4), 280.25, 280.30(2), 307.200; Income Tax Assessment Regulations 1997 (Cth) reg 307.200.02.

[10] Income Tax Assessment Act 1997 (Cth) ss 100.35, 100.40(2), 100.45.

Related insights into tax law

-

Budget bills introduced to House of Representatives

On 28 May 2026, the Commonwealth Government introduced the following two (2) tax reform bills into the House of Representatives: These two (2) Bills have been tabled as part of the Albanese Government’s tax reform package announced in the 2026–27 Federal Budget on 12 May 2026. Minimum CGT Bill The Minimum CGT Bill amends…

-

Federal Budget announces tax on discretionary trusts

On 12 May 2026 the Albanese Labor Government delivered the Federal Budget. They propose to impose of a thirty (30) percent minimum tax on discretionary trusts, commencing 1 July 2028. This article addresses the proposed rate and scope and identifies what remains unclear, particularly how and when the tax will be collected based on the…

-

What are unrealised capital gains?

An unrealised capital gain refers to an increase in the value of an asset that has not yet been sold or disposed of. In Australia, capital gains are taxed on assets which have increased in value when they are sold and the gain is realised, however the proposed Treasury Laws Amendment (Better Targeted Superannuation Concessions)…

-

What exactly are retained earnings?

Retained Earnings are a financial metric that offers a valuable insight into a company’s financial health, extended stability and potential for future growth. They represent the profit a company has retained overtime after accounting for all liabilities including the payment (if any) of dividends.

-

High Court on asset protection – house in spouse’s name

The decision of the High Court of Australia in Bosanac v Commissioner of Taxation [2022] HCA 34 (Bosanac) reaffirms the viability of protecting real property assets by registering them in the name of a spouse.

-

Digital games tax offset introduced by Albanese

The Albanese Labor Government has proposed a Digital Games Tax Offset (DGTO) of 30%, encouraging the growth of the digital games industry in Australia. Learn more about the DGTO and how it will create more jobs and international competitiveness.

-

R&D Tax Incentive and clinical trials

Find out if you are eligible for the Australian Government’s RandD Tax Incentive: companies with an aggregated turnover of

-

Present entitlement in trusts – what it means

Explore the High Court’s interpretation of “present entitlement” under the Income Tax Assessment Act 1936 (Cth). Learn when a person has a vested interest in trust assets and how the trustee’s discretion affects the beneficiary’s entitlement.

-

Software royalties and income tax – explained

Discover how the Australian Taxation Office (ATO)’s draft Taxation Ruling 2021/D4 could affect your business. Learn more about the expanded scope of what is considered a royalty for income tax purposes and the potential tax implications.